Blockchain Technology Explained – For Beginners

What is blockchain? The term became widely popular with the rise of bitcoin. After all, the cryptocurrency’s creator(s), Satoshi Nakamoto, developed the technology to serve as a public distributed ledger for the bitcoin token. But it is more than just securing and storing cryptos.

Our guide fully and clearly explains everything about blockchain technology, how it works, and its many features and benefits. It’s perfect for beginners because we use plain English – no technical jargon.

Blockchain Walkthrough Summary

Here are the main points we discuss in this article:

- Blockchain was created by Bitcoin founder Satoshi Nakamoto.

- It is a decentralized public distributed digital ledger.

- Its purpose is to record and store bitcoin transactions securely.

- The technology can be applied in other fields like banking and finance.

- Benefits include reduced cost, less time, and more robust security.

What Is Blockchain?

The idea of blockchain technology dates back to 1991, when it was still a research project. Its first application served as a digital distributed ledger for bitcoin, the largest cryptocurrency by market capitalization. Think of it as a database for transaction record-keeping and logging.

But unlike traditional databases, blockchain is decentralized. It offers increased security, speed, and cost efficiency when handling transactions without relying on intermediaries or centralized authorities.

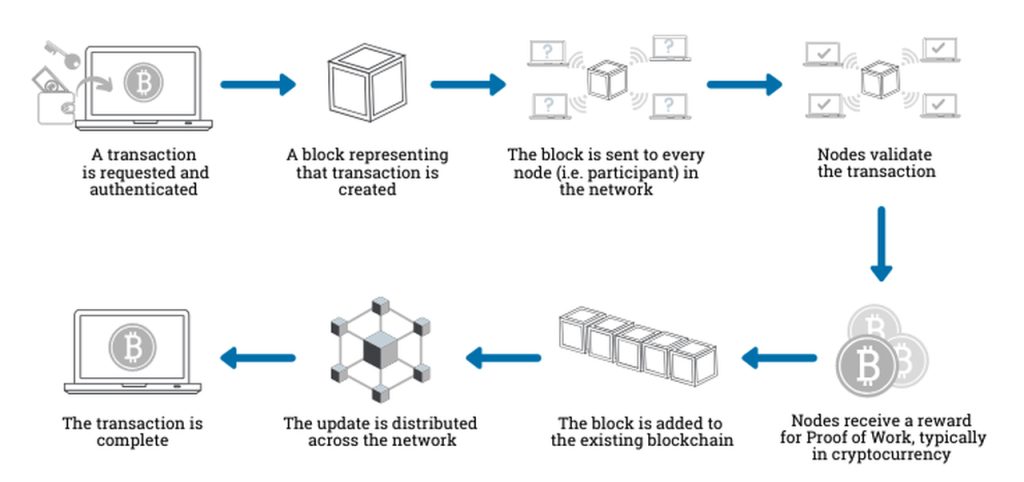

As the name suggests, a blockchain comprises a chain of blocks that collect and log information. Once a block reaches its data storage capacity, it links to other filled blocks via cryptography to form a blockchain. Then, a new block steps in to handle further information and join the network once full.

This structure results in an irreversible data timeline, as each block has its own timestamp. No one can tamper with the registered information because no single entity has total control, contrary to centralized systems.

Instead, all nodes of the blockchain share the data. Any attempt to change it requires the approval of all network participants, a significant advantage in terms of security.

Blockchain Use Cases

Blockchain has been widely popular with cryptocurrencies like Bitcoin and Ethereum as a decentralized digital ledger. But plenty of other industries can implement and benefit from this technology.

- Banking and finance: Transactions take up to three business days when you wire money through your bank, and you can only do so during specified business hours. Blockchain technology handles your request within minutes at lower fees at any time of the day or week.

- Healthcare: Blockchain secures medical records and prevents any form of tampering. These files contain personal, sensitive information that only patients and specific doctors can access with a private key, which ensures privacy.

- Voting: Implementing blockchain into politics is very beneficial. It makes voting more convenient and eliminates potential fraud. No one will be able to tamper with votes, there’s no room for human error or a need for a recount, and results are nearly instant.

- Property records: Recording property rights is both time-consuming and susceptible to human error. To this day, you must physically deliver specific files to government employees who manually enter the data into the database. Blockchain ensures accurate data input instantly.

- Supply chains: The decentralized public ledger allows suppliers to log their purchased materials securely and without data corruption or tampering. As a result, companies can verify the products’ authenticity.

- Shipping: The maritime industry can significantly benefit from blockchain technology. Real-time tracking, reduced workloads, faster and more secure payments, fewer errors, and lower costs are just a few advantages.

Blockchain Pros and Cons

While real-life applications of blockchain technology seem limitless and highly beneficial, it still faces some challenges.

PROS

- Decentralized technology

- Secure, fast transactions

- Full transparency

- No human error

- User privacy

- No intermediaries

- Lower transaction fees

- No data tampering

- Unchangeable logs

CONS

- A high cost of mining

- Low transactions per second

- Could be used by criminals

- Limits on data storage

FAQ

We answer all your blockchain questions.

Who created blockchain?

The idea of blockchain technology dates back to 1991, but it was first implemented in 2009 by bitcoin creator Satoshi Nakamoto, a pseudonym for an unknown person or group of people.

What are the 4 types of blockchain?

There are primarily four types:

- Public

- Private

- Hybrid

- Consortium

What is its main purpose?

Blockchain is a decentralized digital ledger that collects and logs information without allowing any tampering, editing, deleting, or destroying.

What is an example of blockchain?

Blockchain technology is most commonly used for cryptocurrency transactions, such as bitcoin and Ethereum.

What are the top blockchain platforms?

Here are the top platforms for 2023:

- Ethereum

- IBM

- Hyperledger Fabric

- Hyperledger Sawtooth

- Stellar

- R3 Corda

- Tezos

- EOSIO

- ConsenSys Quorum

Conclusion

Although blockchain is primarily a digital ledger for recording and storing cryptocurrency transactions, it has so much more potential. Implementing it brings huge advantages like stronger data privacy and security, no intermediary commission, total decentralization, faster transactions, and zero data tampering.

Some challenges include mining costs (especially bitcoin) and energy consumption. But overall, this technology seems to be the way of the future.

Crypto trading (trading in general, actually) is always a risky business because the industry is volatile. Therefore, make smart choices and don’t invest more than you can afford to lose.

6 thoughts on “Blockchain Technology Explained – For Beginners”